Your Cyber-Insurance Renewal Is Now Your Security Roadmap

Cyber insurance requirements in 2026 turn your renewal questionnaire into a security roadmap. The controls underwriters demand, how to lower premiums, and what to prove.

The renewal questionnaire lands in your inbox at twice the length of last year's, and this time a scan of your perimeter is stapled to it. The carrier set the deadline. The carrier wrote the questions. The carrier ran reconnaissance against your public IP space before you typed a single answer.

That document is the most useful security framework you will touch all year. Every line on it is backed by claims the insurer has paid in cash, every gap it exposes carries a price in premium dollars, and a third party verifies your answers against reality.

Read it as a roadmap and you walk away with a prioritized, externally validated, budget-justified security plan for the cost of a policy you were buying anyway.

The pressure sits on you. You do not control the renewal date, you do not control the questions, and a denied claim after a ransomware hit is an outcome that arrives with your name on it. So stop treating the questionnaire as a hurdle and start mining it.

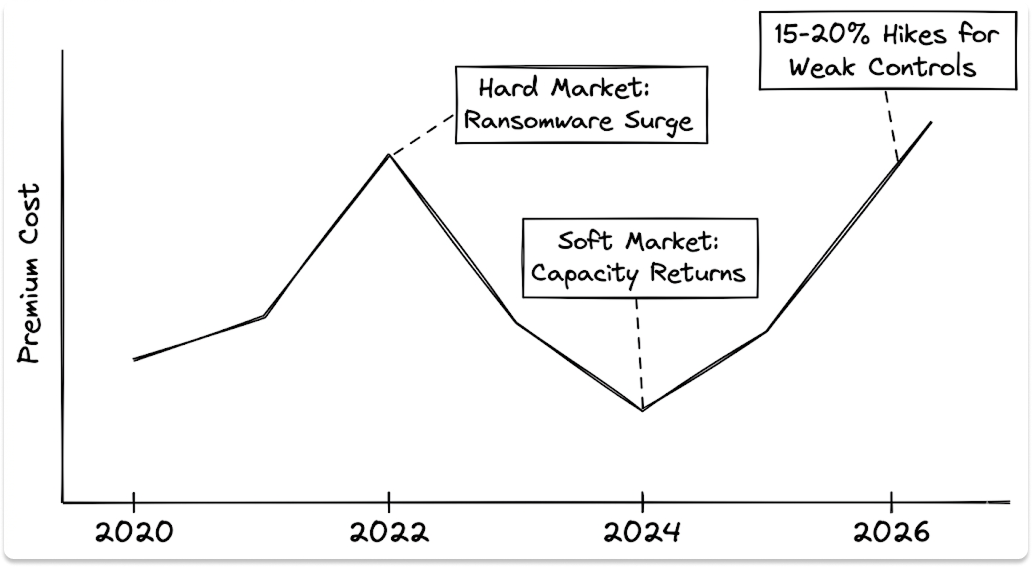

Why cyber insurance underwriting got teeth: the 2022 to 2026 rate cycle

To use the questionnaire well, understand why it got so demanding. The answer is in the rate cycle.

The market moved in three beats. Rates hardened after ransomware exploded in 2020 and 2021, then capacity returned and prices fell 27% from the mid-2022 peak. Buyers spent two years enjoying cheaper coverage and looser terms.

That softening is ending. Analysts now expect premium increases of 15% to 20% in 2026, with the steepest hikes landing on insureds who cannot prove strong technical controls. Loss pressure is climbing underneath, with ransomware frequency up 45% year over year even as average ransom payments fell by half.

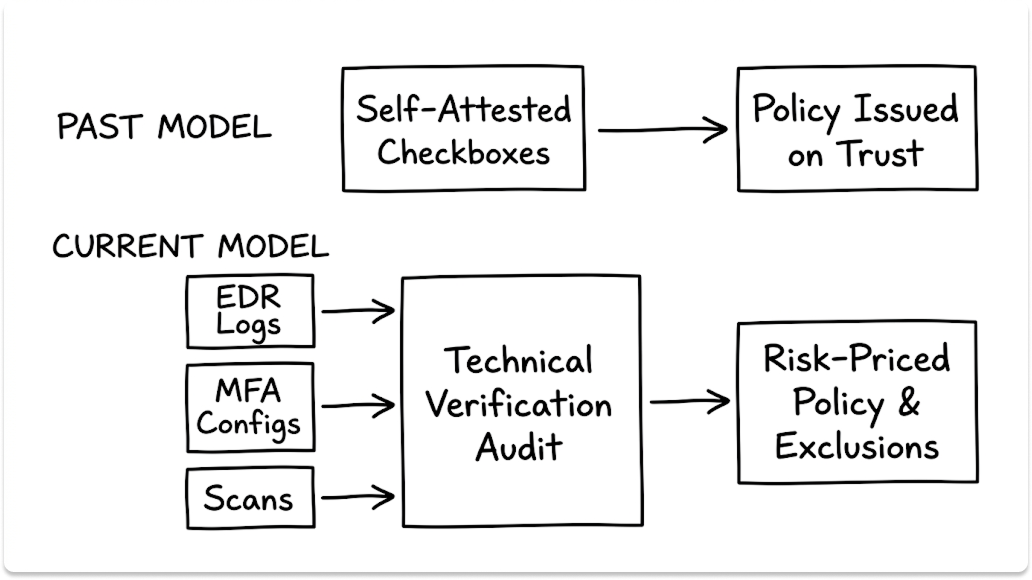

The mechanical change matters more than the pricing. Underwriting moved from self-attested checkboxes to evidence. Underwriters now run their own scanners against your external attack surface, demand proof of specific controls, and write exclusions that void claims if you misrepresented your posture. The questionnaire is a technical audit with money attached.

Your first move, today: run the carrier's reconnaissance before the carrier does. Pull your external footprint and hunt for exposed RDP, expired certificates, and forgotten services. Diff your patch state against the CISA Known Exploited Vulnerabilities catalog. Whatever their scanner surfaces, you want to have found it two weeks earlier and either fixed it or written a remediation note.

The security controls cyber insurers require in 2026

These controls appear on effectively every application now. I have laid out each one the way an underwriter reasons about it: the requirement, the attack it interrupts, the loss data behind it, and the exact artifact you produce to prove it. Answer from the artifact, never from memory.

Multi-factor authentication on every access path

MFA belongs on email, VPN, RDP, SSH, every privileged account, and every cloud console. Phishing-resistant FIDO2 sits at the top of the preference order, app-based authenticators in the middle, SMS at the bottom, because carriers increasingly treat SMS-based MFA as insufficient against SIM-swapping and favor authenticator apps or hardware keys.

This question carries more weight than any other on the form. 82% of cyber insurance claims involved organizations without MFA, and the same report found 41% of applications get denied on first submission, with missing MFA the leading reason. The control earns that weight because the math is lopsided: MFA blocks more than 99.2% of account-compromise attacks.

The common failure is partial coverage. Teams enable MFA on email and leave the VPN on password-only access. Underwriters ask about remote access by name, and a password-only VPN is a red flag.

Action: enforce MFA on remote and privileged access first, this week.

Evidence: a Conditional Access export plus a coverage table by account type showing zero gaps.

EDR or MDR, not legacy antivirus

Signature antivirus scans files against known malware. Intrusions route around it with fileless techniques and living-off-the-land binaries like PowerShell. Endpoint detection and response watches behavior instead: process chains, credential access, lateral movement, command-and-control traffic, flagging anomalies whether or not they match a signature.

Carriers want it on every workstation and server, actively monitored. One unmonitored box is the one that gets encrypted.

Action: reconcile your EDR console headcount against your asset inventory and close the delta before you answer.

Evidence: a console coverage report by operating system and the enrolled percentage across endpoints and servers.

Immutable, tested backups

Ransomware leverage collapses when you can restore. The requirement is immutable or air-gapped backups held off your production identity plane, so one stolen admin credential cannot reach both copies. Documented restore tests with measured recovery time and recovery point objectives complete the ask.

The word underwriters care about is tested. A backup you have never restored is a hypothesis, and they have paid too many claims where the hypothesis failed.

Action: schedule a restore test now and capture the timestamps; an untested backup answers the question with a no.

Evidence: immutability or object-lock configuration and a dated restore-test log showing the RTO and RPO you actually hit.

A tested incident response plan

Carriers want a written plan with assigned roles, exercised through a tabletop inside the last twelve months, plus named contacts for your IR retainer and breach counsel. Insurers want more than a generic disaster recovery document; they want proof you can contain and recover without paying a ransom.

Containment speed drives claim severity directly, which is why this question shapes both eligibility and price.

Action: book a two-hour tabletop and write the after-action report; that single artifact answers several questions on the form.

Evidence: the versioned plan, the tabletop report, and the retainer agreement.

Email authentication and anti-phishing

SPF, DKIM, and DMARC need to be live and enforced. A DMARC record sitting at p=none only monitors; it blocks nothing. The target is p=reject. This control maps to business email compromise, the fraud that drains accounts without ever dropping malware, and BEC has driven more than $55 billion in reported losses since 2013.

Action: move DMARC from p=none to p=quarantine, then to p=reject once your reports are clean.

Evidence: the published policy record at enforcement and a sample aggregate report.

Patch and vulnerability management with defined SLAs

Insurers want documented patch windows, KEV-based prioritization, and no end-of-life software in production. The teeth are in the exclusions. Many policies refuse coverage when a breach exploits a publicly known vulnerability that had a patch available for more than 30 days, enforced hard for KEV entries.

A second trigger bites here too. Running unsupported systems past their end-of-life date can void coverage for incidents tied to those systems. The vendor sets that date, the clock is public, and an unpatched legacy box turns a covered incident into an uncovered one.

Action: pull a list of every EOL asset in production and either retire it or document a compensating control before you sign.

Evidence: your patch SLA, a KEV remediation log with dates, and an inventory confirming no EOL systems.

Privileged access management and network segmentation

These two cap the blast radius. PAM means separate admin accounts, just-in-time elevation, and least privilege, so one stolen credential does not own the domain. Segmentation keeps critical systems and backups off a flat network where ransomware spreads sideways without friction.

Action: strip standing admin rights from daily-use accounts and put backups on their own segment.

Evidence: PAM configuration and admin inventory for the first, a segmentation diagram and firewall ruleset for the second.

Here is the full set in one view.

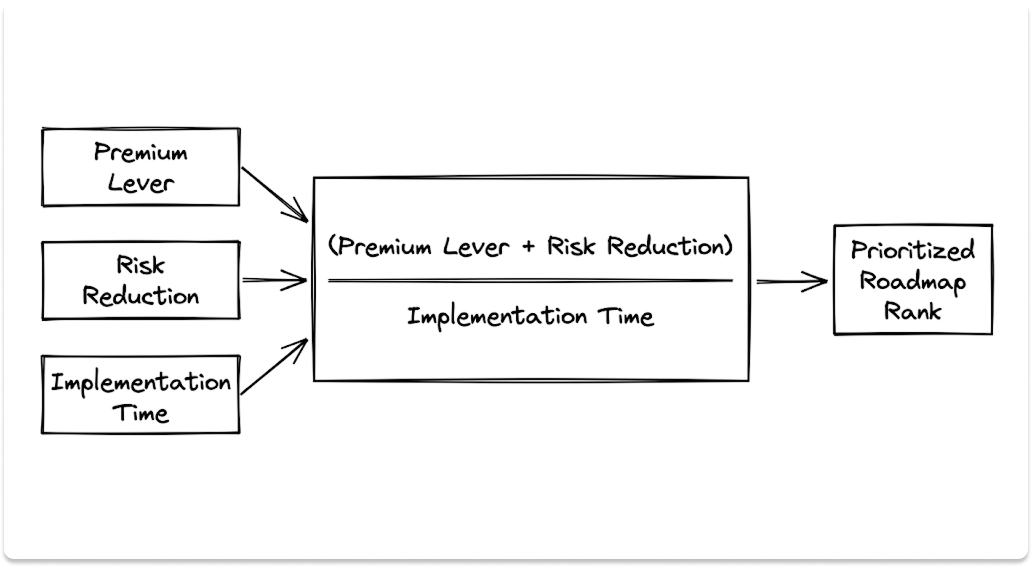

Read the questionnaire as a prioritization engine

A list of controls is not a plan. The value comes from sequencing the gaps, and the questionnaire hands you every input you need to do that.

Score each gap on three axes: its premium and coverage impact, its risk reduction, and its time to implement. Divide the first two by the third and you get a ranking.

MFA, EDR, and immutable backups top the list on every axis, which makes them the right opening moves for any team starting behind. They are also the fastest to stand up, so they convert into lower risk and better terms inside one cycle.

The premium impact is concrete. Carriers attach measurable credits to controls above the baseline: a 24/7 managed SOC can earn 10 to 15%, FIDO2 MFA 5 to 10% over app-based MFA, annual penetration testing 5 to 10%, and SOC 2 Type II 10 to 20%. Run the logic in reverse and inaction sharpens: businesses with control deficiencies pay 50 to 200% more, when they can get coverage at all.

Turn that into the artifact you bring to finance and the board. Build a gap register where every row carries a security justification, a loss statistic, and a dollar figure on closing or leaving the gap.

Each row closes a gap an actuary already priced, which is the strongest budget case you can put in front of a CFO. Pull your broker into this early; ask them which carriers reward your strongest controls, and steer the gap register toward the credits that move your specific renewal.

The attestation trap: what you are actually signing

Evidence-based underwriting turned the signature on that application into a legal instrument, and the case law is settled enough to hurt.

In 2022, an electronics manufacturer attested to MFA on administrative and privileged access. The company actually ran MFA only on its firewall while leaving its servers exposed, and those servers were the target of the ransomware attack.

After the breach, the policy was rescinded. The application carried the signature of the CEO and the head of network security, which killed any argument that the company misunderstood what it had deployed.

Intent is not the safeguard people assume. A federal appeals court reaffirmed in 2024 that a material misrepresentation, intentional or not, lets an insurer rescind a policy from inception.

An honest mistake voids coverage the same way a lie does. The court tests whether the statement was false and whether it was material to the underwriting decision.

A second exposure catches careful teams. Your policy assumes you keep the controls you attested to. Disable EDR to troubleshoot a performance issue, get breached during that window, and the insurer can argue you failed to maintain a material condition. You can pass in March and lose the protection in August without changing a word on the form.

Operate by three rules and you stay clear of all of it:

- Answer every question from exported evidence. If the screenshot does not show it, you do not have it.

- Log a compensating-control memo for any honest no, with the gap, the interim mitigation, and a remediation date. Underwriters take honesty plus a plan over a false yes.

- Let only the person who can prove the answer sign it. Keep non-technical signers off technical attestations.

From annual scramble to continuous control assurance

The companies that win the best terms can show their work on demand, which means breaking the once-a-year fire drill.

Stand up an evidence repository and keep it current all year. Hold your Conditional Access policies, EDR configurations, backup immutability settings, patch SLAs, and the last twelve months of training and phishing-simulation records in one folder. When renewal arrives, you assemble a folder instead of reconstructing a year.

Map each question to one control and one live evidence source, then reconcile the numbers. Mismatches between what your application states and what your tooling shows are a top cause of underwriting delay. If the policy declares 200 endpoints and your EDR console shows 240, fix that before an underwriter finds it.

Set drift alerts so your attested state stays true between renewals. Flag new MFA exclusions, drops in EDR enrollment, and failed backup jobs, because each one is a silent slide from covered to exposed.

Work the calendar backward from your renewal date. Plan 60 to 90 days end to end, since controls take one to eight weeks to deploy and a clean application with controls already in place clears underwriting in two to four. A workable runbook:

- Day 90: self-scan, build the gap register, pull your broker in.

- Day 75 to 30: run remediation sprints, lead with MFA, EDR, and immutable backups.

- Day 30 to 10: assemble the evidence folder and reconcile every device count.

- Final week: attest from artifacts, with compensating-control memos attached for any remaining gaps.

The cheapest external audit you will ever run

Strip away the policy language and the renewal is an actuarially priced, externally verified read on your real risk posture. The carrier already ranked which controls prevent losses, attached a price to each gap, and scanned your perimeter to check your claims. Few internal audits deliver that, and none deliver it for the cost of coverage you were buying anyway.

The payoff reaches past the premium line. Cyber-insured companies have watched loss impacts rise about 70% over four years against 250% for uninsured peers, and the ten-year ROI of coverage runs near 19%. Companies that meet the controls get breached less and recover faster when they do.

So spend the cycle building the program and let the policy fall out as the byproduct. The questionnaire told you what to fix, ranked it, and priced it. Treat it as the roadmap it already is, and start with the gap at the top of your register before the deadline starts working against you.

Renewal questionnaire exposing gaps you can't close in time?

Compare MFA, EDR, backup, and incident-response partners from a catalog of pre-vetted vendors, filtered to the controls your policy now demands. Match with the ones that fit and start conversations when you're ready. You stay anonymous until you reach out. And it's free.

FAQ

What are the cyber insurance requirements for 2026?

Most carriers now require eight core security controls before binding coverage: multi-factor authentication across email, VPN, RDP, and admin accounts; EDR or MDR instead of legacy antivirus; immutable, tested backups; a tested incident response plan; SPF, DKIM, and DMARC at enforcement; documented patch SLAs with no end-of-life software in production; privileged access management; and network segmentation. Underwriters ask for evidence of each, not just a yes.

Why is MFA mandatory for cyber insurance?

Multi-factor authentication is the single most weighted control on the application because the claims data is lopsided. Coalition found 82% of cyber insurance claims involved organizations without MFA, and MFA blocks more than 99.2% of account-compromise attacks. Carriers increasingly want phishing-resistant FIDO2 or app-based MFA rather than SMS, and enforced on remote and privileged access specifically.

How do I lower my cyber insurance premium?

Close the control gaps underwriters price against, then document them. Controls above the baseline carry measurable credits: a 24/7 managed SOC, FIDO2 MFA, annual penetration testing, and SOC 2 Type II certification each reduce premiums. Conversely, missing controls raise costs 50 to 200% or trigger a declination, so the fastest savings come from MFA, EDR, and immutable backups.

Can a cyber insurance claim be denied for misrepresenting security controls?

Yes. If you attest to a control you do not actually have, the insurer can rescind the policy from inception after a breach, and intent does not matter. A material misrepresentation, even an honest mistake, is grounds for rescission. You can also lose coverage by disabling an attested control, like turning off EDR, and getting breached during that window. Always answer from exported evidence.

How long does it take to meet cyber insurance requirements before renewal?

Plan 60 to 90 days end to end. Individual controls take one to eight weeks to deploy, and a clean application with controls already in place clears underwriting in two to four weeks. A workable sequence: self-scan and build a gap register at day 90, run remediation sprints from day 75 to 30, assemble and reconcile evidence from day 30 to 10, and attest from artifacts in the final week.